Cities, counties, and states across the U.S. are showing that transparency is always a good thing—especially for our buildings. With a growing number of energy benchmarking policies causing more owners and operators of large buildings to measure, track, and share their energy use, we’re gaining better insights into how we can improve performance and save more energy.

A 2012 EPA analysis revealed that 35,000 buildings, benchmarked with ENERGY STAR Portfolio Manager, had an average energy savings of 7 percent over three years compared to a 2008 baseline. There are several obvious benefits to saving energy in buildings, including using the money saved on utility bills for upgrades and maintenance, reducing greenhouse gas emissions, and increasing energy security. However, a less-evident benefit, and one that deserves a thorough examination, is the greater financial value of properties that invest in energy efficiency.

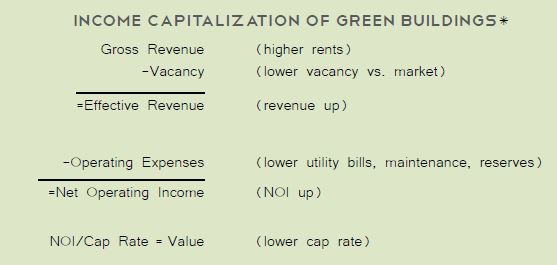

There are generally three accepted methods appraisers use to determine how much money a commercial building is worth – income capitalization, cost comparison, and comparable sales. To determine the financial value of green buildings, the best method for appraisers to use is income capitalization—which calculates value from a building’s net operating income (NOI), as illustrated in the following chart.

Chart: IMT, 2014

Referencing the above income capitalization chart, we start by investigating how energy benchmarking and transparency policies can affect a building’s effective revenue, which is calculated by taking a building’s gross revenue (the money earned if the building were 100-percent occupied) and subtracting the unrealized revenue due to vacancy. By increasing the transparency of building energy use, benchmarking policies incentivize building owners to invest in energy efficiency in order to make their buildings more attractive to potential renters and the public.

Studies have shown that rental premiums exist for green commercial buildings, and so energy efficiency investments may allow owners to charge higher rental rates to their tenants. An increasing number of tenants are also willing to pay more for space in high-performing buildings, as leasing green space can support an organization’s commitment to sustainability, attract employees, and increase worker comfort and productivity.

In addition to driving higher rents, energy efficiency investments can affect vacancy rates. Green commercial buildings command occupancy premiums, and thus energy-efficient buildings are likely to have lower vacancy compared to their more conventional peers. So looking back up at the chart, we see that greater gross revenue (from higher rental rates) and lower vacancy gives us a very positive effective revenue for building owners.

Another piece of the puzzle and a clear benefit from investing in energy efficiency is a reduction in building operating expenses due to lower energy bills. The income capitalization chart shows that reduced operating expenses, combined with greater effective revenue, leads to an overall increase in NOI. The last step in calculating building value is dividing NOI by the local capitalization rate, or cap rate, a process known as direct capitalization.

Cap rates describe annual property income as a percentage of property value, and they vary across real estate markets. The cap rate is not unlike the price-to-earnings ratio—and like that metric for evaluating stocks, the cap rate is a measure of assets’ expected risk and return. Lower cap rates reflect a more valuable asset—In 2013 the urban multifamily asset class led across markets in the U.S., with a 5.76 percent cap rate, per industry consultant Integra.

This approach to valuing green buildings – the income capitalization approach – is the preferred method of property valuation, due in part to the relatively low number of comparable green properties, and it is an effective way to explain how energy benchmarking policies can improve the financial performance of commercial properties. However, it is one thing to talk about the income-based approach to green building valuation and quite another to see it used in the marketplace.

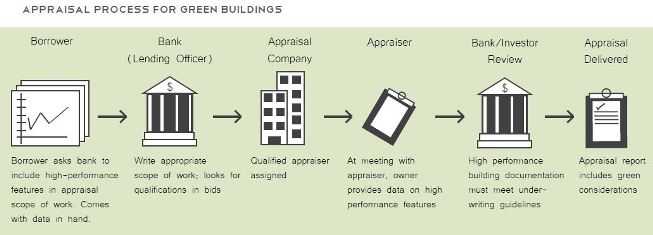

The green appraisal process relies on the motivation and experience of three key stakeholders: the building owner, the bank, and the appraiser. The following flowchart details the important roles played by each stakeholder:

Graphic: IMT, 2014

The building owner, or borrower, must be actively engaged in the process of obtaining a green appraisal. It is important for the owner to select a bank that has experience dealing with green buildings and then request that the bank include the building’s high-performance features in the appraisal scope of work. If possible, the bank should then select a qualified appraiser with experience valuing green buildings, such as a professional certification through the Appraisal Institute, which now offers an education track and certification in valuing green buildings. Throughout the green appraisal process, the owner should be prepared to provide the bank and appraiser with data on the building’s high-performance features. These actions are key to the success of a green appraisal in practice.

Energy benchmarking and transparency policies help owners provide banks and appraisers the necessary information to value energy efficiency. In this way they are a catalyst to several beneficial outcomes in the real estate sector. While greenhouse gas emissions and energy security receive substantial attention, the financial benefits that arise from benchmarking policies should not be discounted, and in fact more effort should be directed towards properly valuing high-performing buildings.

For a more in-depth look at the appraisal process and how green, high-performance characteristics and data can be used by appraisers to help fully maximize valuation, read IMT and the Appraisal Institute’s paper, “Green Building and Property Value.”